What is the definition, scope, and significance of the North America Transformer Monitoring System Market?

The North America Transformer Monitoring System Market encompasses advanced technologies designed to continuously assess the health and performance of power and distribution transformers across the region. These systems integrate hardware sensors with IT solutions to monitor critical parameters including bushing condition, oil and gas composition, temperature, and load levels. The market scope covers utilities, industrial facilities, and renewable energy installations requiring reliable power infrastructure. Significance stems from aging grid infrastructure, increasing electricity demand, and the critical need to prevent unplanned outages. Transformer failures can cost millions in damages and downtime, making predictive monitoring essential for grid reliability, asset optimization, and regulatory compliance across the United States, Canada, and Mexico.

What are the key drivers, restraints, challenges, and opportunities in the North America Transformer Monitoring System Market?

Key drivers include aging transformer fleets averaging 30-40 years old, rising electricity consumption, smart grid investments, and stringent reliability regulations. The transition to renewable energy creates variable loads requiring advanced monitoring. Restraints involve high initial deployment costs, integration complexity with legacy systems, and cybersecurity concerns for connected devices. Challenges include interoperability standards gaps, skilled workforce shortages for data analytics, and utility budget constraints. Opportunities emerge from IoT-enabled sensors, AI-driven predictive analytics, digital twin technologies, and condition-based maintenance programs. The market benefits from federal grid modernization funding, increasing adoption of online dissolved gas analysis, and growing demand for bushing monitoring solutions across distribution and power transformer applications.

What current and emerging trends are shaping the North America Transformer Monitoring System Market?

Current trends include widespread adoption of online dissolved gas analysis (DGA) for oil/gas monitoring, increasing deployment of bushing monitoring systems using capacitance and tan delta measurements, and integration of hardware sensors with cloud-based IT solutions for real-time analytics. Emerging trends feature AI and machine learning algorithms for predictive failure detection, digital twin implementations for asset lifecycle management, and edge computing for localized data processing. The shift toward condition-based maintenance over time-based schedules drives demand for continuous monitoring. Wireless sensor networks reduce installation costs, while cybersecurity-hardened communication protocols address grid vulnerabilities. Modular, scalable solutions allow utilities to prioritize critical transformers first, expanding monitoring coverage incrementally across distribution and power transformer fleets.

How did COVID-19 impact the North America Transformer Monitoring System Market and what is the recovery trajectory?

COVID-19 initially disrupted supply chains for monitoring hardware components and delayed field installations due to workforce restrictions and utility capital expenditure reductions in 2020. However, the pandemic accelerated digital transformation priorities, highlighting the value of remote monitoring capabilities when physical inspections were limited. Utilities recognized the need for resilient, remotely manageable grid assets, driving renewed investment in transformer monitoring systems. The recovery trajectory shows strong momentum as deferred maintenance programs restart and grid modernization funding increases. Post-pandemic focus on infrastructure resilience, coupled with federal stimulus packages targeting energy infrastructure, supports sustained growth. The market demonstrates resilience with monitoring solutions now considered essential rather than optional for critical transformer assets.

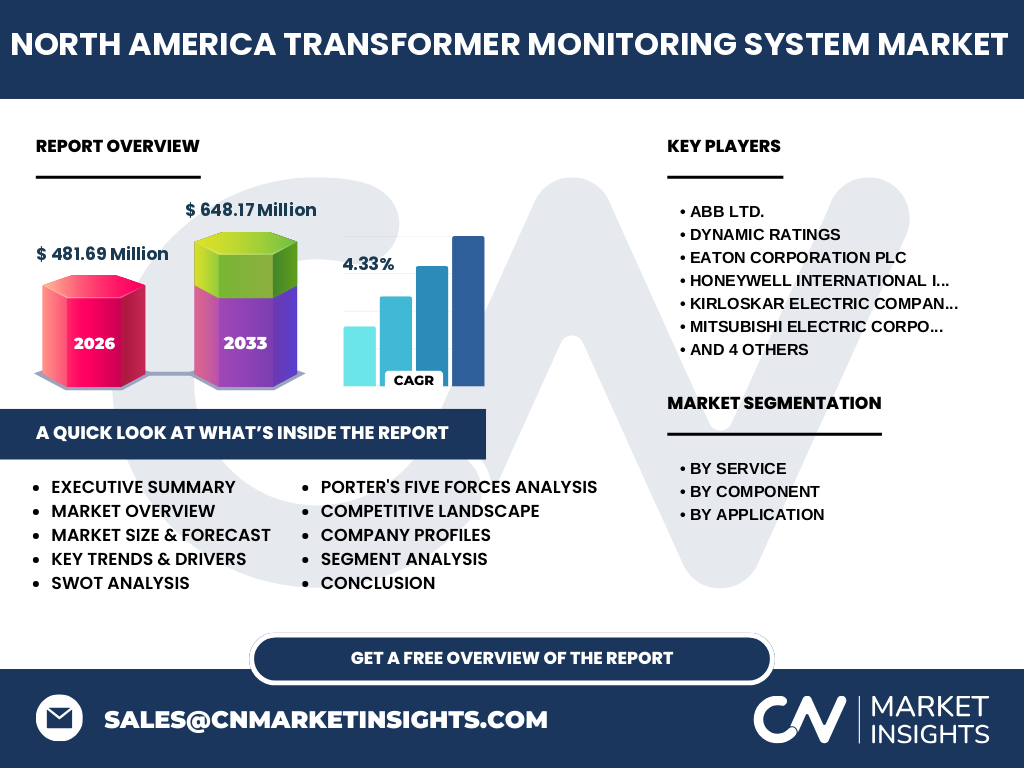

Who are the major competitors and what is the competitive landscape in the North America Transformer Monitoring System Market?

The competitive landscape features established global electrical equipment manufacturers and specialized monitoring solution providers. Key companies include ABB Ltd., Siemens AG, Schneider Electric SE, Eaton Corporation plc, Honeywell International Inc., Mitsubishi Electric Corporation, Schweitzer Engineering Laboratories, Inc., Dynamic Ratings, Kirloskar Electric Company, and Wilson Transformer Company. Competition centers on integrated hardware-software platforms, sensor accuracy, analytics capabilities, and utility relationship depth. Large players leverage broad product portfolios and global service networks, while specialists like Dynamic Ratings and Schweitzer Engineering Laboratories focus on niche monitoring technologies and advanced analytics. Market consolidation continues through strategic partnerships and acquisitions targeting complementary technologies, particularly in IT solutions, AI analytics, and cybersecurity-enhanced monitoring platforms for both distribution and power transformer applications.

What are the key findings and high-level overview of the North America Transformer Monitoring System Market?

The North America Transformer Monitoring System Market demonstrates steady growth driven by aging infrastructure, grid modernization imperatives, and increasing reliability requirements. The market size reaches 481.69 Million in 2026, with forecasts projecting 648.17 Million by 2033, representing a 4.33% CAGR. Growth is fueled by both service segments - bushing monitoring and oil/gas monitoring - across hardware and IT solution components. Applications span distribution transformers and power transformers, with utilities prioritizing critical assets. Key players including ABB, Siemens, Schneider Electric, and specialized providers compete on integrated platform capabilities. The market benefits from regulatory support, technological advancement in sensors and analytics, and shifting maintenance paradigms toward condition-based approaches, positioning sustained expansion through the forecast period.

What are the market projections for the North America Transformer Monitoring System Market from 2025 to 2032?

The North America Transformer Monitoring System Market shows consistent growth trajectory with the market size reaching 481.69 Million in 2026 and forecasted to reach 648.17 Million by 2033, reflecting a compound annual growth rate of 4.33%. This growth projection accounts for increasing utility investments in grid reliability, aging transformer fleet management, and adoption of advanced monitoring technologies across both distribution and power transformer segments. The forecast period encompasses continued deployment of bushing monitoring and oil/gas monitoring services, expansion of hardware sensor networks, and growing integration of IT solutions for data analytics and predictive maintenance. Market expansion supports condition-based maintenance programs, regulatory compliance requirements, and the ongoing transition toward smart grid infrastructure across the United States, Canada, and Mexico.

How is the North America Transformer Monitoring System Market segmented by service, component, and application?

The market segmentation reveals three primary dimensions. By service, the market divides into bushing monitoring and oil/gas monitoring, addressing distinct failure modes in transformer insulation systems. By component, the market separates into hardware - including sensors, communication modules, and data acquisition units - and IT solutions encompassing analytics software, visualization platforms, and integration middleware. By application, the market covers distribution transformers serving end-user loads and power transformers handling bulk transmission, each with unique monitoring requirements and criticality levels. This segmentation reflects the diverse technical needs across the transformer fleet, with utilities selecting monitoring combinations based on asset criticality, age profile, and failure risk. The segmentation framework enables targeted solution deployment and informs product development strategies for market participants.

What is the geographic distribution of the North America Transformer Monitoring System Market across regions?

The North America Transformer Monitoring System Market encompasses the United States, Canada, and Mexico as the primary geographic regions. The United States represents the largest market share driven by extensive aging transformer infrastructure, significant utility capital expenditure programs, and federal grid modernization initiatives. Canada follows with substantial investments in hydroelectric and renewable integration requiring advanced transformer monitoring. Mexico shows growing demand from grid expansion and reliability improvement programs. Regional variations exist in regulatory frameworks, utility structures, and technology adoption rates. The market analysis considers each country's unique grid characteristics, transformer fleet demographics, and investment climates while recognizing the integrated nature of North American power markets and cross-border transmission interconnections influencing monitoring requirements.

What are the detailed regional market performances within North America for transformer monitoring systems?

Regional analysis reveals distinct market dynamics across North America. The United States leads with the most mature monitoring deployments, driven by investor-owned utilities, municipal utilities, and cooperatives managing extensive transformer fleets. Major regional transmission organizations (RTOs) and independent system operators (ISOs) impose reliability standards accelerating adoption. Canada's market emphasizes hydroelectric generator step-up transformers and long-distance transmission assets, with provincial utilities investing in comprehensive monitoring. Mexico's market grows from CFE modernization programs and private sector participation in generation and transmission. Regional differences in climate extremes, load growth patterns, and regulatory environments create varied monitoring priorities - from wildfire-prone areas requiring enhanced bushing monitoring to regions with high renewable penetration needing advanced power transformer analytics.

Who are the leading companies in the North America Transformer Monitoring System Market and what are their strategies?

Leading companies include ABB Ltd., Siemens AG, Schneider Electric SE, Eaton Corporation plc, Honeywell International Inc., Mitsubishi Electric Corporation, Schweitzer Engineering Laboratories, Inc., Dynamic Ratings, Kirloskar Electric Company, and Wilson Transformer Company. Strategies differentiate between integrated platform providers and specialized monitoring experts. ABB, Siemens, Schneider Electric, and Eaton leverage full electrical portfolios, offering monitoring as part of comprehensive asset management suites with global service networks. Honeywell and Mitsubishi Electric emphasize industrial IoT integration and advanced analytics. Schweitzer Engineering Laboratories and Dynamic Ratings focus on protection-grade monitoring with deep power system expertise. Kirloskar and Wilson Transformer Company bring transformer manufacturing heritage to monitoring solutions. Competitive strategies center on sensor innovation, analytics sophistication, cybersecurity, and utility partnership models.

What does Porter's Five Forces analysis reveal about the North America Transformer Monitoring System Market?

Porter's Five Forces analysis indicates moderate to high competitive intensity. Threat of new entrants remains moderate due to high technical barriers, utility qualification requirements, and established incumbent relationships. Bargaining power of suppliers is moderate, with specialized sensor component providers holding some leverage while IT solution providers face competitive software markets. Buyer power is significant - large utilities consolidate purchases, demand integration capabilities, and require long-term support commitments. Threat of substitutes exists from manual inspection programs and basic SCADA monitoring, though these lack predictive capabilities of dedicated systems. Competitive rivalry is intense among established players differentiating on analytics depth, sensor accuracy, total cost of ownership, and service responsiveness. The market structure favors incumbents with proven utility track records and integrated hardware-software platforms.

What are the strengths, weaknesses, opportunities, and threats in the SWOT analysis of the North America Transformer Monitoring System Market?

Strengths include proven technology reducing catastrophic failures, strong utility relationships among incumbents, regulatory tailwinds for grid reliability, and advancing sensor/analytics capabilities. Weaknesses involve high upfront costs challenging smaller utilities, integration complexity with legacy systems, cybersecurity vulnerabilities in connected devices, and data overload without actionable analytics. Opportunities emerge from federal infrastructure funding, aging transformer replacement cycles, renewable integration requiring enhanced monitoring, AI-driven predictive maintenance, and expanding distribution transformer monitoring. Threats include utility budget cycles and regulatory uncertainty, potential technology obsolescence, competitive price pressure, supply chain disruptions for specialized components, and skilled workforce gaps for advanced analytics. The SWOT profile supports continued investment in integrated, scalable solutions addressing both transmission and distribution transformer monitoring needs.

How does the value chain analysis structure the North America Transformer Monitoring System Market?

The value chain encompasses component suppliers providing sensors, communication modules, and processing hardware; system integrators assembling hardware-software platforms; software developers creating analytics, visualization, and integration solutions; distributors and channel partners reaching utility customers; and end-users including investor-owned utilities, municipal utilities, cooperatives, and industrial facilities. Value flows from raw component manufacturing through platform development to deployment services, ongoing maintenance, and analytics subscriptions. Key value-add stages include sensor calibration for accuracy, algorithm development for predictive insights, cybersecurity hardening, and utility-specific customization. The chain features feedback loops where operational data improves algorithms, driving continuous value enhancement. Strategic partnerships between hardware specialists, analytics providers, and utility engineering firms create integrated offerings addressing the full monitoring lifecycle from installation to actionable intelligence.

What are the strategic investment insights for the North America Transformer Monitoring System Market?

Key investment insights highlight prioritizing integrated hardware-software platforms over point solutions, as utilities seek single-vendor accountability. Investments in AI-driven analytics for predictive failure detection offer differentiation and recurring revenue potential. Cybersecurity-hardened architectures address critical utility concerns and regulatory requirements. Scalable, modular solutions enabling phased deployments reduce utility adoption barriers. Distribution transformer monitoring represents an underpenetrated segment with massive asset counts. Partnerships with transformer manufacturers enable embedded monitoring in new units. Geographic focus on regions with oldest transformer fleets and aggressive grid modernization programs maximizes addressable market. Investment in interoperability standards compliance (IEC 61850, DNP3) reduces integration friction. Services revenue from managed monitoring and analytics subscriptions creates annuity streams beyond initial hardware sales.

What are the summary conclusions and key takeaways for the North America Transformer Monitoring System Market?

The North America Transformer Monitoring System Market presents a compelling growth story with 4.33% CAGR projecting expansion from 481.69 Million in 2026 to 648.17 Million by 2033. Fundamental drivers - aging infrastructure, reliability mandates, and digital grid transformation - create sustained demand across bushing monitoring, oil/gas monitoring, hardware, and IT solutions for both distribution and power transformers. Competitive dynamics favor integrated platform providers with proven utility deployments. Critical success factors include actionable analytics over raw data, cybersecurity by design, scalable deployment models, and deep utility engineering partnerships. The market transitions from reactive to predictive maintenance paradigms, with monitoring becoming standard practice for critical assets. Stakeholders should anticipate continued consolidation, technology convergence, and expanding monitoring scope across the transformer fleet.

What research methodology was used to analyze the North America Transformer Monitoring System Market?

The research methodology employs a multi-phase approach combining primary and secondary research. Primary research includes structured interviews with utility asset managers, transformer monitoring system vendors, system integrators, and regulatory experts across the United States, Canada, and Mexico. Secondary research encompasses utility regulatory filings, capital expenditure reports, transformer fleet demographics, IEEE and CIGRE technical publications, vendor financial disclosures, and government infrastructure program announcements. Market sizing utilizes bottom-up modeling based on transformer population data, monitoring penetration rates, and average system pricing across segments. Forecast modeling incorporates macroeconomic indicators, utility capital planning cycles, technology adoption curves, and policy scenario analysis. Data triangulation across sources ensures accuracy, with validation through expert review panels and sensitivity analysis on key assumption variables.

What is the research scope and coverage limitations for the North America Transformer Monitoring System Market analysis?

The research scope covers the North America Transformer Monitoring System Market across the United States, Canada, and Mexico for the period spanning 2025-2033. Coverage includes all major market segments: by service (bushing monitoring, oil/gas monitoring), by component (hardware, IT solutions), and by application (distribution transformers, power transformers). Key companies analyzed include ABB Ltd., Dynamic Ratings, Eaton Corporation plc, Honeywell International Inc., Kirloskar Electric Company, Mitsubishi Electric Corporation, Schneider Electric SE, Schweitzer Engineering Laboratories, Inc., Siemens AG, and Wilson Transformer Company. The analysis encompasses market size, growth trends, competitive landscape, regulatory environment, and technology evolution. Financial projections use the provided market size of 481.69 Million for 2026 and forecast of 648.17 Million by 2033 at 4.33% CAGR as baseline metrics for all quantitative assessments.

What are the key companies and their recent developments in the North America Transformer Monitoring System Market?

Key companies driving market developments include ABB Ltd. advancing Ability™ transformer monitoring with AI analytics, Siemens AG expanding SITRAM portfolio with digital twin integration, Schneider Electric SE enhancing EcoStruxure Asset Advisor for transformer fleets, Eaton Corporation plc developing IntelliNet monitoring with grid-edge analytics, Honeywell International Inc. integrating Forge platform for industrial transformer monitoring, Mitsubishi Electric Corporation deploying MELCO monitoring with advanced DGA interpretation, Schweitzer Engineering Laboratories, Inc. advancing SEL-TMU with synchrophasor integration, Dynamic Ratings innovating in bushing monitoring and thermal modeling, Kirloskar Electric Company leveraging manufacturing expertise for integrated monitoring solutions, and Wilson Transformer Company expanding condition monitoring services. Recent developments focus on cloud-native platforms, cybersecurity certifications, utility pilot program expansions, and strategic partnerships between hardware specialists and analytics providers accelerating time-to-value for transformer monitoring deployments.